After a turbulent spring in municipal bonds, we believe the market should give investors reasons for optimism as we approach summer. The muni underperformance we saw in May should make for fertile ground in the coming months.

Municipal bond market investors faced a surprisingly challenging May. A confluence of stronger-than-expected economic data, sticky inflation, and sensational headlines around a potential US government default made for an uncertain spring. In addition, a few muni-specific technical factors—namely abundant muni supply, weak reinvestment demand, and the liquidation of high-quality muni holdings from select regional banks in receivership—dovetailed with the trajectory of US Treasury yields to produce today’s elevated muni yields.

This potent combination, along with unexpectedly resilient economic data and uncertainty around future Federal Reserve action on interest rates, sparked what we consider a muni “flash sale.” Ten-year benchmark tax-exempt yields vaulted to their highest levels year-to-date (YTD) while also underperforming corresponding-maturity US Treasuries and registering the highest muni-to-Treasury value ratios of the year. But, as often happens, we believe a turbulent spring and today’s yields could lead to some promising summer performance for bondholders.

What might summer bring to muni markets?

We believe the months ahead should provide a tailwind for current bondholders. First, the prevailing value in munis has set the stage for outperformance in June, July, and August, possibly taking relative 10-year benchmark muni-to-Treasury value ratios—currently in the low-70% range—into the mid- to high-50% levels. For context, the average YTD ratio is 65%, with a high of 73% and a low of 59%. We believe summer value ratios could even challenge the record low of 55%, set in February 2021 at the height of the pandemic.

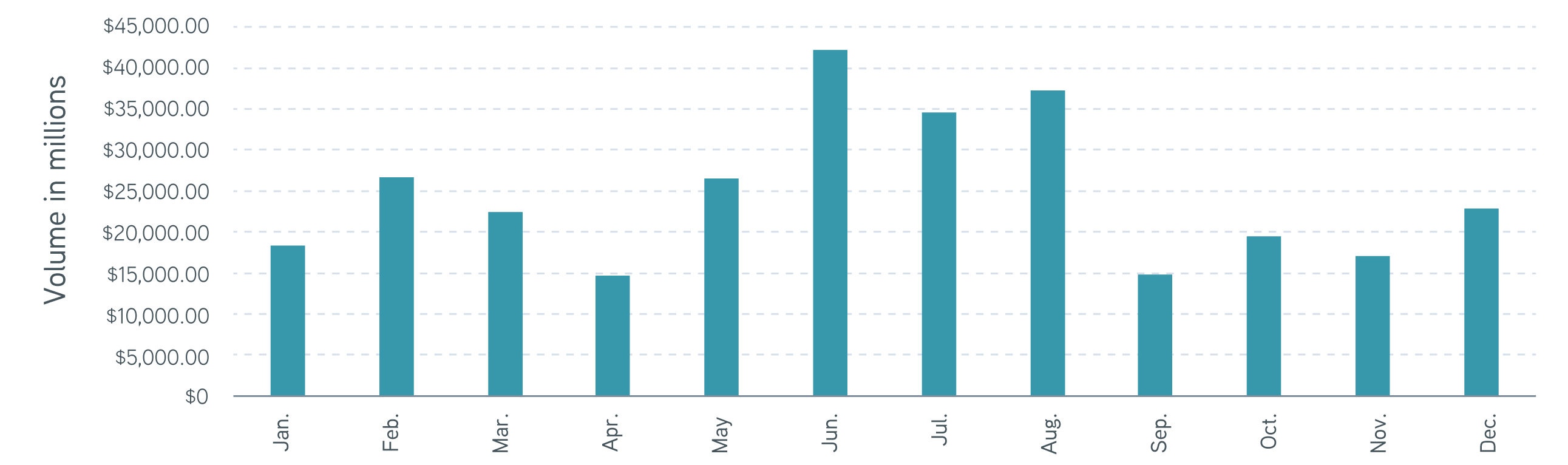

According to ICE data, the three summer months are typically the busiest of the year for maturing bonds, called bonds, and coupon payments hitting existing bondholder accounts. Projected June redemptions alone amount to more than $42 billion—a 55% uptick from May—and the combined three-month projected total for the summer is more than $114 billion. We expect much of this prospective reinvestment cash will find its way back into tax-exempt munis, driven by more attractive bond yields than we’ve seen in recent years. In addition, the Fed did ultimately announce its mid-June decision to halt interest rate hikes, at least for the time being.

Projected total 2023 muni redemptions

Source: Intercontinental Exchange, Inc., 5/31/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. Forecasts and estimates are based on current market conditions, are subject to change, and may not necessarily come to pass.

Solutions for today’s complex interest rate environments

Will muni bond supply meet demand?

It seems unlikely. Summer new-issue supply calendars historically feature some of the lightest primary market supply of the year. Supply is already down almost 25% YOY through May, according to the Bond Buyer. We expect negative net supply to fuel muni outperformance as more dollars chase fewer bonds, even if we assume consistent issuance at the recent run rate of $7 billion per week. The Fed’s announced rate-hike inaction may calm things some, but with recent economic data coming in mixed to above-consensus expectations, we believe elevated yields and continued volatility may present an opportunity for muni investors to get ahead of the strong summer technical factors before they fully take hold.

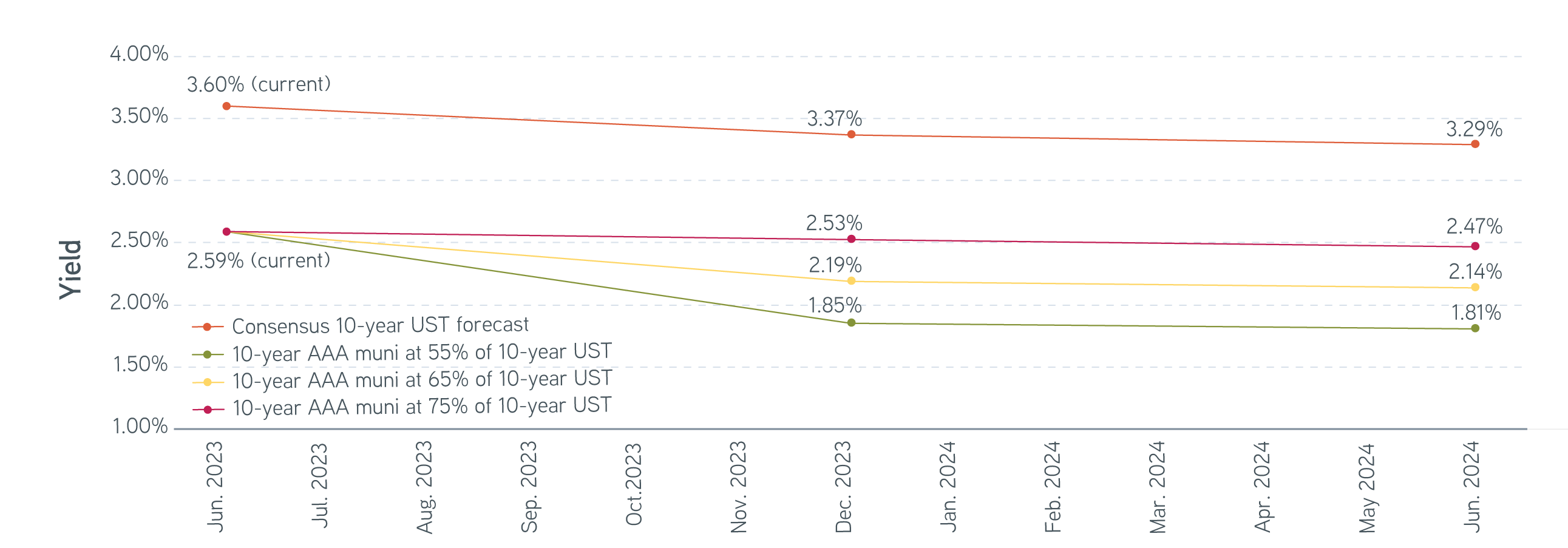

Looking ahead, if we multiply the Street consensus forecast yield for 10-year US Treasuries (according to Bloomberg) by three potential relative value ratios—0.75, 0.65, and 0.55—we see three possible paths for the current 10-year benchmark AAA muni yield. While that forecast model produces three different outcomes for the next year, they’re all price positive compared with our June starting point, even without considering coupon income—a major component of total return for municipal bonds. For example, if we look at the 55% relative value scenario (the green line in the following figure) and assume a muni coupon of 5% (the most prevalent structure YTD), the prospective gain on price change alone (based on the US Treasury forecasts) for year-end 2023 and midyear 2024 amounts to approximately 4.97% and 4.35%, respectively. And when we include coupon income, the potential for positive returns is even more impressive, at 7.87% and 9.43%, respectively.

Rate forecast, munis vs. US Treasuries

Sources: Bloomberg, Refinitiv MMD, 6/1/2023. For illustrative purposes only. Does not represent actual returns of any investor and should not be relied on for investment decisions. Forecasts and estimates are based on current market conditions, are subject to change, and may not necessarily come to pass. All investments are subject to risks, including the risk of loss of principal. Please refer to the disclosures included at the end of this material for additional important information.

The bottom line

After May’s perfect spring storm of stronger-than-expected economic data, persistent inflation, and the panic around the perceived debt-ceiling crisis, we see summer presenting a very different dynamic in the municipal bond market. We expect today’s currently elevated yields and continued volatility, followed by net negative supply over the summer, to fuel material muni outperformance. The US economy is proving itself resilient, and we believe muni bond market investors are in a strong position to take advantage of today’s opportunities before summer technicals take hold.