This year, market participants responded to the fears that initially developed in 2022, resulting in a year of seesawing yields. But we think 2024 will be anticipatory, with investors positioning themselves early in the year to weather out any storm. Learn why we think the bond market is favorably aligned for a new year.

This year has been a bit more tumultuous than we had envisioned, but it wasn’t quite as difficult as the calamitous 2022. We expected 2023 to be a transition year, with the themes of recession, rates, and returns. Perhaps pandemic-related distortions have taken longer to move through the economy than we forecasted. Inflation proved more stubborn and the economy more robust than we anticipated for much of this year, which contributed to a higher-for-longer bias in rates.

If our key themes for 2023 are only now coming to pass as we head toward 2024, what then to say about the year to come? With apologies to Fleetwood Mac fans, we say, “Don’t stop thinking about tomorrow.” If 2023 was reactionary, with market participants responding to the fears that emerged in 2022 and yields seesawing on data, then we think 2024 will be anticipatory. Market participants could become more convinced of the imminence of rate cuts and position themselves with greater conviction. In short, 2024 could be the year of FOMO.

What happened in fixed income in 2023?

In our opinion, some of the trends we anticipated may have been delayed. Returns may be back, since both the Bloomberg Municipal Bond Index and the Bloomberg US Aggregate Index have moved into positive territory in the fourth quarter. November is poised to be the strongest month of the year for these indexes, and December technicals favor further strength.

Rates may have peaked. The Federal Open Market Committee (FOMC) didn’t raise rates at its December 13 meeting, going six months with holding rates steady. While inflation remains above target, signs of a clear disinflationary trend have emerged. Consumer Price Index (CPI) year-over-year (YOY), running at 6.4% in January, was down to 3.2% in October. The unemployment rate hit a multi-decade low of 3.4% in January and inched up to 3.9%. The rate of increase in average hourly earnings has also dropped from 4.7% to 4.1%.

Recession remains a remote prospect, though, with the US economy continuing to post steady growth. The Atlanta Fed GDPNow forecast is calling for growth around 2.0% for the final quarter of the year. An inverted yield curve has historically been a reliable indicator of an impending recession, but the unique circumstances of the pandemic may have undone that. The jury is out.

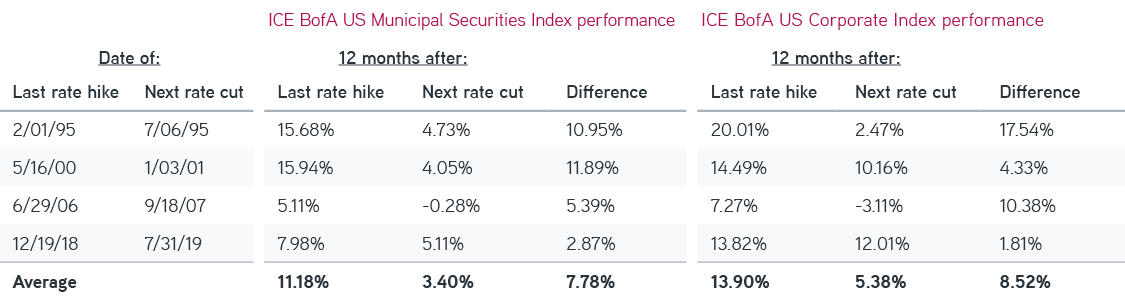

When could investors get into bonds in 2024?

While there’s some uncertainty as to the timing of an entry point, being early has delivered exceptional returns in the past. Over the past 30 years, the 12-month period following the last rate hike has produced very attractive municipal and corporate bond returns. The table below shows the returns on the BofA US Municipal Securities Index and the BofA US Corporate Index over the 12 months following the last rate hike and the 12 months following the first rate cut. Investors benefited from acting sooner rather than later in each period. With 10-year US Treasury rates already 50 basis points (bps) lower than their recent October highs, we think the incentives are good for investors to put cash to work today.

Solutions for today’s complex interest rate environments

Muni and corporate fixed income index performance after rate-hiking cycles

Sources: Bloomberg, ICE, 11/30/2023. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses. Past performance is not indicative of future results.

Conditions in the municipal market could be supportive of performance in 2024 with fewer bonds around and supply declining. After a 21% YOY drop in annual issuance in 2022, 2023 YOY annual issuance was running lower yet again, down 8% year-to-date through October. Yields are off their highs, but they remain among the most attractive they’ve been in a decade. At the end of November, the yield to worst of the ICE BofA Municipal Securities Index was 3.75%—higher than at the end of 2022 and well above its 10-year average of 2.32%.

Credit conditions are good, with municipalities that built up reserves during the pandemic by and large maintaining them. Tax receipts have grown along with the economy. Should a recession occur, we see most issuers as well positioned to weather one without significant credit deterioration. However, it’s always best practice to conduct ongoing credit monitoring.

Tighter spreads and the positive ratings trend are two additional indicators that credit conditions and the overall economic outlook remain healthy for investment-grade (IG) corporate bonds. The best financial metrics are likely behind us as higher rates slowly work their way into IG companies’ income statements. Even so, interest coverage remains strong at 12.3 times, well above the levels seen prior to the last four recessions. The first-quarter collapse of some regional banks sparked concern that a broader banking crisis could develop. These fears have largely faded, and corporate spreads are now at a YTD low of 120 bps, 18 bps tighter on the year but still 34 bps above their 2021 low.

Rating agencies remain optimistic on the corporate bond sector as well, upgrading a record $134 billion of BBB bonds to A this year. The BBB portion of the corporate bond index fell from 51.5% in March 2021 to 47.0% at the end of October as a result. This improvement comes despite $64 billion of high-yield bonds transitioning to the BBB index following a ratings upgrade in 2023. Many of these rising stars were previously IG companies, and their upgrade has reduced the size of the ICE Fallen Angel Index as a percent of the ICE High Yield Index to a record-low 6%. These numbers don’t include an additional $41 billion of debt from a major automaker, which recently became the largest rising star on record.

What’s ahead for fixed income in 2024?

We find ourselves pretty optimistic about next year. That said, investors may become concerned that this rate cycle will develop in a materially different manner than previous ones. Four months have passed since the last Fed rate hike on July 26 without a cut. During the last four hiking cycles, the time between the last hike and the first cut ranged from five to 14 months.

The Fed has expressed its commitment to bringing inflation down to its 2% target and that this goal may require keeping rates higher for longer. Should an anticipated rate cut not happen in 2024, yields could once again have an upward trajectory. While this outcome would likely disappoint many, ladder investors could benefit from higher reinvestment rates while they wait for yields to normalize.

Higher rates would provide another opportunity for tax-loss harvesting (TLH), which can be used to offset equity gains and potentially reduce an investor’s current or future tax obligations. The conditions of 2023 are a good example of why we recommend year-round TLH. Unless rates rise substantially in December, an investor who waited until year-end to recognize losses would have missed out on the better opportunities earlier in the year.

The bottom line

Though entry points are never certain, getting into fixed income early has historically yielded great results for investors. We believe that risks and rewards are favorably aligned and that the most likely outcome is that 2024 could be a good year for bond investors.