If you’re not sure what direct indexing means, you’re not alone. Even after the recent growth, direct indexing remains relatively unknown. As our compliance team never fails to remind us, you can’t invest directly in an index. So what exactly is direct indexing?

The first thing to note is that the name may be relatively new, but the strategy isn’t. In fact, direct indexing describes what Parametric has been doing for over 30 years: providing an alternative to index mutual funds and passive ETFs for investors who want more choice, greater flexibility and the potential tax advantages that those commingled investments simply can’t offer.

Direct indexing has been in the news a lot more in recent years. Larger industry players have strategically acquired a number of providers—including Parametric. And many new entrants have entered the space, looking to build on its success.

I’ve written many blogs over the years highlighting some use cases of direct indexing, diving into the details of tax management and risk. But I want to use this opportunity to take a step back, to define direct indexing, to answer some common questions and to help advisors and their clients understand who may stand to benefit the most from it.

What is direct indexing?

Most of us are familiar with mutual funds and passive exchange-traded funds (ETFs), which package underlying securities into a single vehicle accessible to investors. Anyone who purchases shares in a passive index-tracking ETF can gain broad market exposure to the benchmark of their choice— for example, the S&P 500®, the Russell 3000® and so on.

Direct indexing takes this idea in a different direction. Instead of owning shares in a commingled fund, the investor owns the individual securities in the portfolio directly, in a separately managed account (SMA). The investor gets the same kind of broad market exposure but with compelling advantages, including the potential to improve after-tax outcomes. For example, unlike an ETF, direct indexing allows investors to customize their portfolios to actively harvest capital losses from individual securities. We’ll talk more about this below.

What are some advantages of customization?

Direct indexing, done right, also unlocks the power of other customizations that allow investors who want broad market exposure to step outside what an index provider decides should be in their portfolios. For instance:

- If the investor has social or environmental principles they’d like to express, they can adjust their holdings to screen out certain industries or companies whose business practices they object to.

- If they have a concentrated position in a particular company’s stock, they can avoid redundant or risk-compounding holdings in their portfolio.

- If they have convictions about certain types of securities—those considered value or momentum stocks, say—they can employ direct indexing to tilt their allocation to favor those characteristics or factors.

- If they need to combine multiple benchmarks to achieve the precise exposure they seek, they aren’t limited to a single benchmark.

In other words, direct indexing takes the one-size-fits-all approach of commingled investing and turns it on its head. This helps advisors add compelling value to a passive portfolio and tailor it to each individual client’s circumstances and values.

What’s more, direct indexing’s direct ownership of individual securities offers powerful flexibility around charitable giving and estate planning. And direct indexing isn’t limited to equities. You can build a direct indexing custom SMA using fixed income, too.

Does all this customization mean direct indexing isn’t truly a passive form of investing? Some subscribe to this reasonable point of view, arguing instead that direct indexing is a unique form of active investing. Regardless of what label we apply, it’s clear that investors increasingly seek ways to capture market-like or beta returns on their own terms—an index of sorts that they can build and control.

Help clients get the precise exposure they seek

Why is tax loss harvesting such an important part of direct indexing?

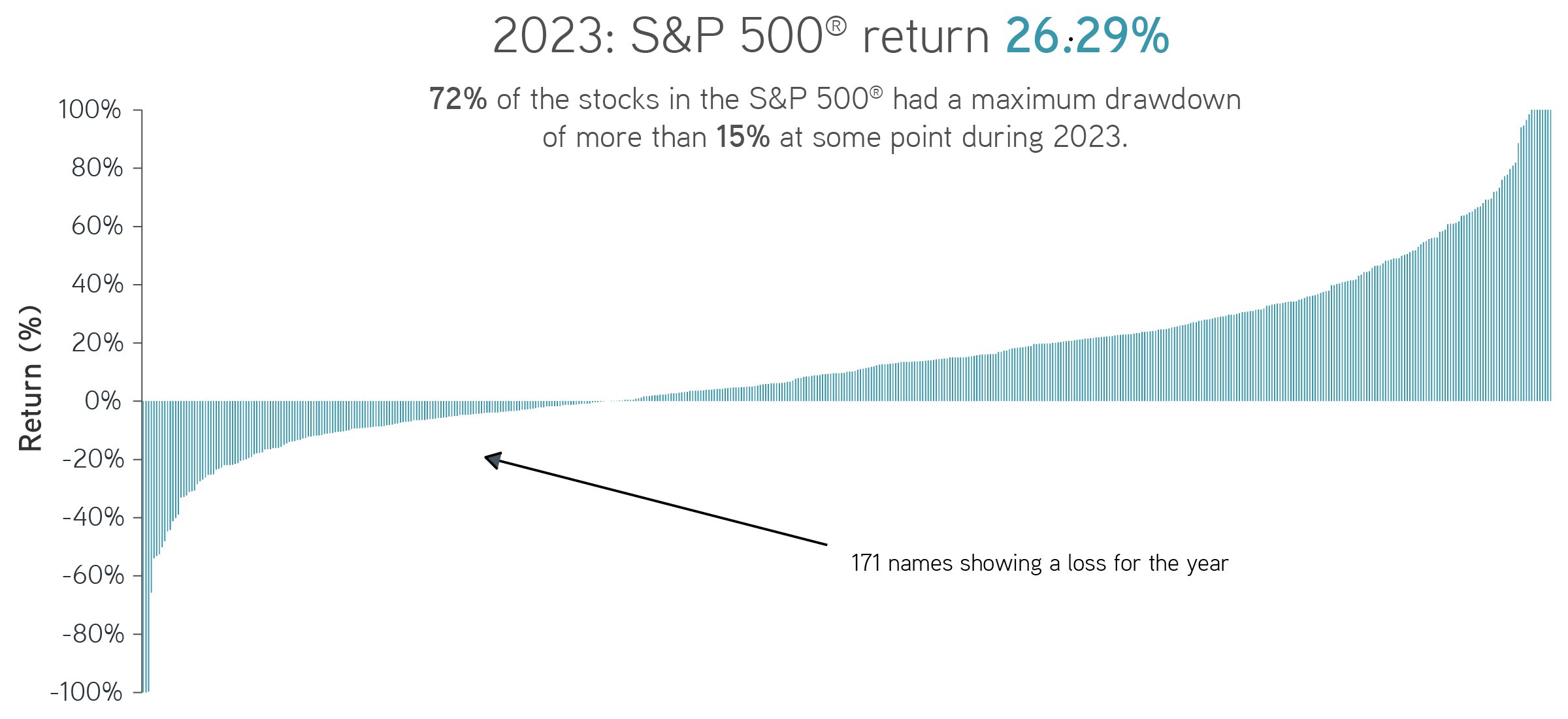

Losses aren’t the goal of any portfolio, and investors generally don’t like to see negative signs in monthly statements—no matter how inevitable they might be in a broadly diversified allocation to stocks or bonds. Even during periods when the broad market and many individual stocks rise in value, quite a few others fall. Here’s an example from 2023, using the S&P 500® Index as a benchmark.

S&P 500® performance in 2023

Source: FactSet, 12/31/2023. This information is for illustrative purposes only and is not a recommendation or an offer to buy, sell, or hold any security. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses. All investments are subject to risks, including the risk of loss. Past performance is not indicative of future results.

Overall, 2023 was a good year for equities. Despite market uncertainty about rising inflation and ongoing global conflicts, the S&P 500® rose more than 26% for the year. Nevertheless, 171 stocks in the index showed a loss for 2023, and over 70% of those names were down at least 15% at some point during the year.

Index fund investors in 2023 couldn’t use those losses to offset capital gains elsewhere in their holdings because they couldn’t access them. The losses were locked in the fund. And investors who sold shares would be on the hook for any required capital gains taxes resulting from that fund unit sale.

By contrast, as I touched on above, when investors own securities directly rather than owning them indirectly, via shares in a fund, they can put those individual losses to work. The SMA portfolio manager can harvest a loss in a given security, and the investor can bank the loss to use in current or future tax years. Then the manager can reinvest the sale proceeds in a similar security—taking care to avoid IRS wash-sale rules—to preserve the investor’s exposure and risk-return profile.

We think a lot about taxes because investors think a lot about taxes. But many investors and their advisors may not be aware that taxes can be a bigger drag on portfolio performance than fees or trading costs. That’s why we don’t wait for the end of the year to begin harvesting losses. To make sure our clients aren’t missing out on opportunities, we harvest losses systematically, throughout the year. Third-party research has shown that tax management can add 1%–2% in after-tax excess returns.1

Is direct indexing right for all investors?

Direct indexing’s benefits can vary depending on an investor’s profile, but the types of investors who may see the greatest value from it include those who:

- Are in a higher tax bracket, so they may have more taxes to save

- Have a long-term investment focus, so they may reap more benefits from tax deferral

- Express convictions about responsible investing, so they may appreciate values-related customization

- Fund a portfolio with existing securities, so they may see real tax savings over selling all positions and reinvesting in a commingled fund

Those whose profiles don’t align with one or more of these traits might not see as many benefits to direct indexing—especially after taking costs into account. Compared with commingled vehicles such as ETFs, custom passive SMAs have higher fees and more operational complexity. And because direct indexing involves customizing the broad market allocation, performance can deviate from the investor’s chosen benchmark returns—often referred to as tracking error. Investors seeking to take advantage of direct indexing’s benefits must be willing to tolerate some carefully managed tracking error.

For these reasons, many investors who don’t naturally benefit from customization may continue to get market exposure through funds and passive ETFs. But we would stress that funds, passive ETFs, direct indexing and even active management aren’t mutually exclusive: All have important roles to play in the investment ecosystem.

The bottom line

Direct indexing continues to grow in popularity and expand its range of use cases. More and more investors are beginning to see the potential benefits of direct indexing, which can be a powerful tool to help them take greater control of their broad market holdings, while realizing more after-tax value from them. The hype has been fun to watch, but at Parametric we’re just happy that a strategy we pioneered and refined over the past 30 years is increasingly being discovered.

1 Shomesh E. Chaudhuri, Terence C. Burnham and Andrew W. Lo, “An Empirical Evaluation of Tax-Loss-Harvesting Alpha.” Financial Analysts Journal, Q3 2020, 76:3, 99–108. This study did not involve Parametric or its clients. There is no guarantee that a tax-management strategy will result in increased after-tax returns. Results will differ based on an individual investor’s circumstances.

Parametric and Morgan Stanley do not provide legal, tax or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy.