Commodity markets have enjoyed a solid rally to start the year after a disappointing finish to 2023. The Bloomberg Commodity Index, a widely recognized proxy for the asset class, rose nearly 7% through the end of May, lifted by strength across nearly all segments except grains.

As we move into the second half of 2024, let’s take a look at a familiar market dynamic that’s often misunderstood in commodity investing: Current inventory levels may be much tighter than futures curves are signaling. Historically, tight inventories have often been associated with better performance for the asset class—but also greater volatility.

Surplus pricing illusion

Back in the summer of 2022, we observed a confluence of supply-side constraints brought on by the pandemic and Russia’s invasion of Ukraine, which sent raw material prices to new records. Simultaneously, this environment pushed commodity futures markets significantly into backwardation—a phenomenon where spot prices trade at a substantial premium to futures prices. The opposite state is referred to as contango, where spot prices trade below futures prices.1

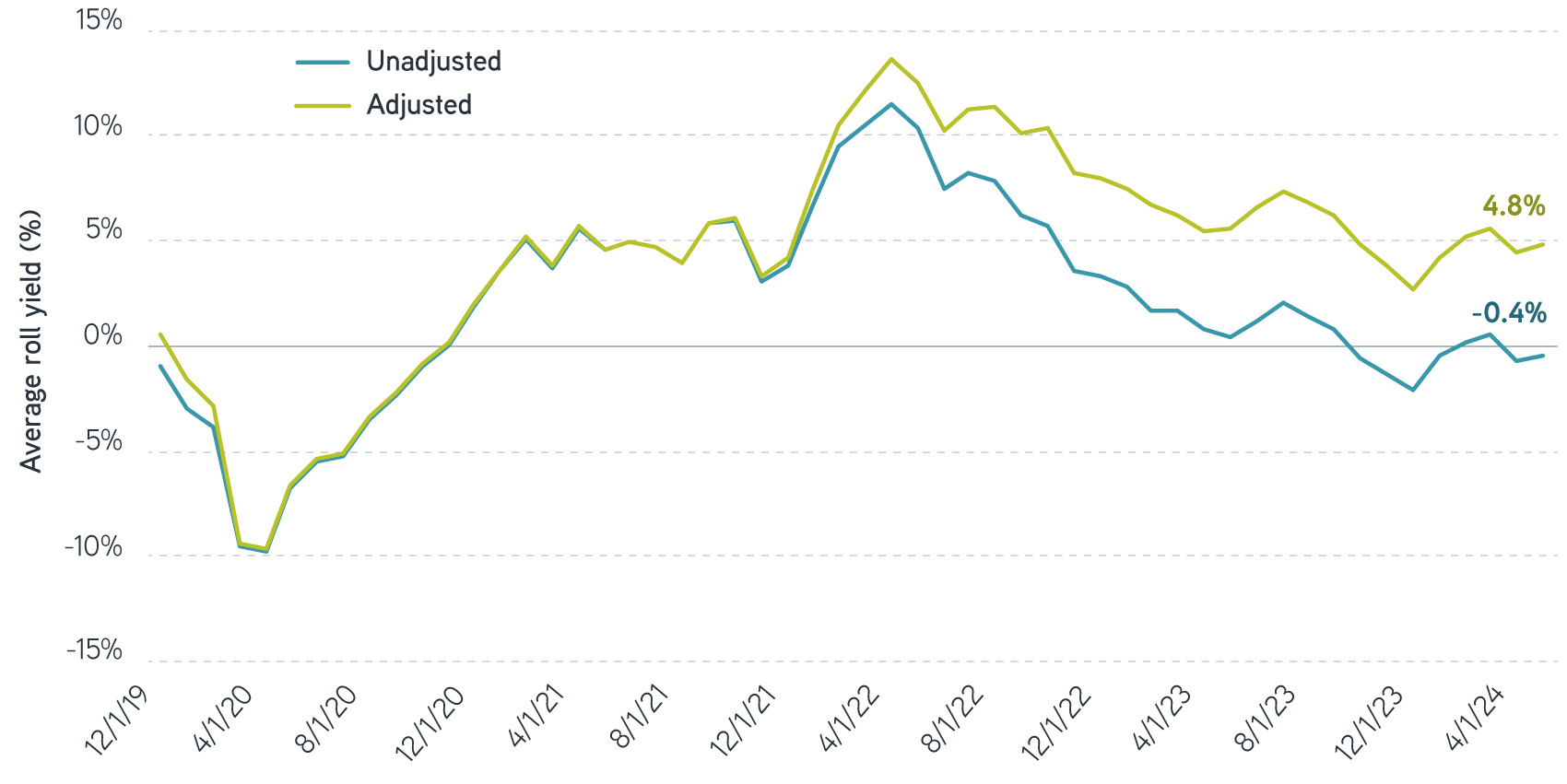

Today, these effects seem to have dissipated. Commodity markets overall appear to be trading with a slight degree of contango. As of May 31, the average level was roughly -0.4%.

A market in contango would suggest that near-term supplies of a commodity are sufficient to meet current demand. Contango is typically observed during periods of surplus inventory in physical raw materials and often unfairly carries a negative connotation related to investment prospects of the asset class.

Role of interest rates in futures pricing

We think it’s worth remembering that interest rates play an important role in setting futures prices. Under normal market conditions, futures prices are higher than spot prices because they incorporate costs that a seller would incur for buying and financing the commodity. Said another way, interest rates contribute to the steepness of the futures curve. As interest rates rise, futures prices appear more expensive relative to spot prices—the futures curve steepens. That means the degree of contango in commodity futures has increased with the increase in rates, which can potentially mask what’s going on in the physical market.

Undoubtedly, the US Federal Reserve’s aggressive moves to raise interest rates in response to recent inflation helps to explain why commodity markets shifted from backwardation to contango over the past two years. As recently as late 2021, the yield on a 12-month Treasury Bill was effectively zero. Today, it’s well over 5%.

To strip out the impact of rising yields and get a better sense of the underlying inventory conditions, we can adjust the futures curve by adding back an equivalent Treasury yield. After this adjustment, we find that the average level of backwardation is actually around 5%. This is unusually high from a historical perspective—on par with conditions earlier in this inflation cycle. In effect, the present adjusted level of backwardation implies that inventories remain relatively tight across many commodities.

Average degree of contango (-) or backwardation (+), January 2019 – May 2024

Sources: Bloomberg, Parametric, 5/31/2024. Roll yield is the difference between the profit or loss of a futures contract and the change in the spot price of the contract’s underlying asset. For illustrative purposes only. Not a recommendation to buy or sell any security. Past performance is not indicative of future results. All investments are subject to risks, including the risk of loss.

Risk management solutions for uncertain markets

Inventory impacts on investors

For commodity investors, the level of inventories can have a big impact on prices. Undersupplied markets tend to be more vulnerable to demand shocks, which may drive prices higher.

We’ve seen this play out recently with copper. Inventories tracked by the COMEX exchange, the primary futures market for copper traded in the US, totaled 24,400 tons as of April 30. For comparison, annual US copper demand is almost two million tons. Solid demand and shipping issues at the Panama and Suez canals, which restrict the ability to move spare copper inventory around the globe, have left the market tight. Consequently, US copper imports are down 15% year over year according to the CRU Group, while copper prices have increased by about 20%.

Another potential consequence of relatively low inventories is higher volatility across commodity markets. In this environment, small shifts to the balance of supply and demand tend to have an outsized effect on the price of a commodity.

Take cocoa as an example. Crop disease and erratic weather patterns have crippled cocoa bean production in Ghana and the Ivory Coast, which account for around two-thirds of the world’s production. The International Cocoa Organization expects supply to fall by 11% to 4.5 million metric tons in 2023–2024, contributing to a potentially catastrophic shortage of the crop. In response, we’ve witnessed extreme moves in the cocoa market, with prices moving up and down by more than 15% on some days.

Over time, higher prices brought on by low inventories can incentivize commodity producers to invest in bringing new supplies to market. But this process can take many months or even years, often complicated by internal and external forces along the way.

The bottom line

Backwardation and contango are the yin and the yang of the commodity futures market. While the post-pandemic period of backwardated commodity markets appears to have given way to modest levels of contango, rising interest rates have been a key driver of this outcome. Underlying supply and demand conditions remain far from balanced.

We believe this trend is noteworthy for commodity investors, because periods of physical market scarcity have historically been associated with better performance on average. In addition, heightened price volatility may continue to impact commodity markets. In our view, that risk may be addressed through broad diversification across the asset class and disciplined rebalancing.

1 It’s common to measure the degree of backwardation or contango by calculating the percentage difference between the futures contract that’s nearest to maturity and the contract maturing in a year. Using this methodology, a positive percentage denotes backwardation, while a negative percentage denotes contango.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.