Weekly Fixed Income Update

Interest rates, inflation, central bank action—all these and more can impact fixed income. Stay on top of the market with our weekly update.

April 30, 2024

Macro update

Last week’s data releases featured manufacturing, durable goods and personal consumption expenditures (PCE)—the Federal Reserve’s preferred metric on inflation. Core PCE came in at 2.7% year over year and 0.3% month over month (Bloomberg, 4/26/2024).

First-quarter GDP data was also released last week and showed that the US economy slowed to a 1.6% growth rate compared with a 2.5% expectation. Despite the slower growth, persistent inflation has likely slowed the Fed’s plan to reduce the overnight interest rate (Bloomberg, 4/26/2024).

This week we have a Federal Open Markets Committee (FOMC) meeting, where the markets expect the overnight rate to remain unchanged. The market will also digest jobs data from April and expect nonfarm payrolls to increase by 240,000 (Bloomberg, 4/26/2024).

Fixed Income Five by Kevin Lynyak

Municipal bond update

Benchmark AAA muni yields increased mildly again last week. Two-, five- and 10-year yields were seven basis points (bps) higher, while 30-year yields rose only six bps (Refinitiv MMD, 4/26/2024).

The Bloomberg Municipal Bond Index again lost 0.29% last week, placing year-to-date (YTD) performance at -1.69%. The Bloomberg US Treasury Index lost 0.2%, taking YTD performance to -3.24% (Bloomberg, 4/26/2024).

Municipal mutual funds reported $200 million of inflows for the week. Open-end mutual fund outflows of $387 million were more than offset by ETF inflows totaling $588 million (JPMorgan, 4/26/2024).

Five-, 10- and 15-year A-rated municipal yields were 3%, 3.12% and 3.64%, respectively, as of the April 26 close. Related taxable-equivalent yields were 5.07%, 5.27% and 6.15%, respectively, assuming the highest rate of federal tax of 40.8% (Refinitiv MMD, Parametric, 4/26/2024).

Corporate bond update

US investment-grade (IG) corporate yields were mixed across the curve last week. Two- and five-year yields fell seven bps and four bps, respectively, while 10-year yields increased by three bps. Corporate yields are higher across the curve YTD, with two-, five- and 10-year yields up 41, 60 and 67 bps, respectively (Bloomberg, 4/26/2024).

The ICE BofA 1–10 Year US Corporate Index returned 0.11% for the week and -1.26% month to date (MTD). The index outperformed like-duration Treasurys on an excess-return basis by 0.19% for the week and 0.21% MTD (Bloomberg, 4/26/2024).

IG mutual funds and ETFs experienced outflows of $46 million, a decrease from last week’s inflows of $901 million. Corporate-only funds experienced outflows of $897 million following last week’s outflows of $1.6 billion (JPMorgan, 4/26/2024).

Corporate one-to-10-year IG bond yields have risen 60 bps YTD and ended last week at 5.7%, a YTD high (Bloomberg, 4/26/2024).

Investing in fixed income securities involves risk. All investments are subject to loss. Learn more.

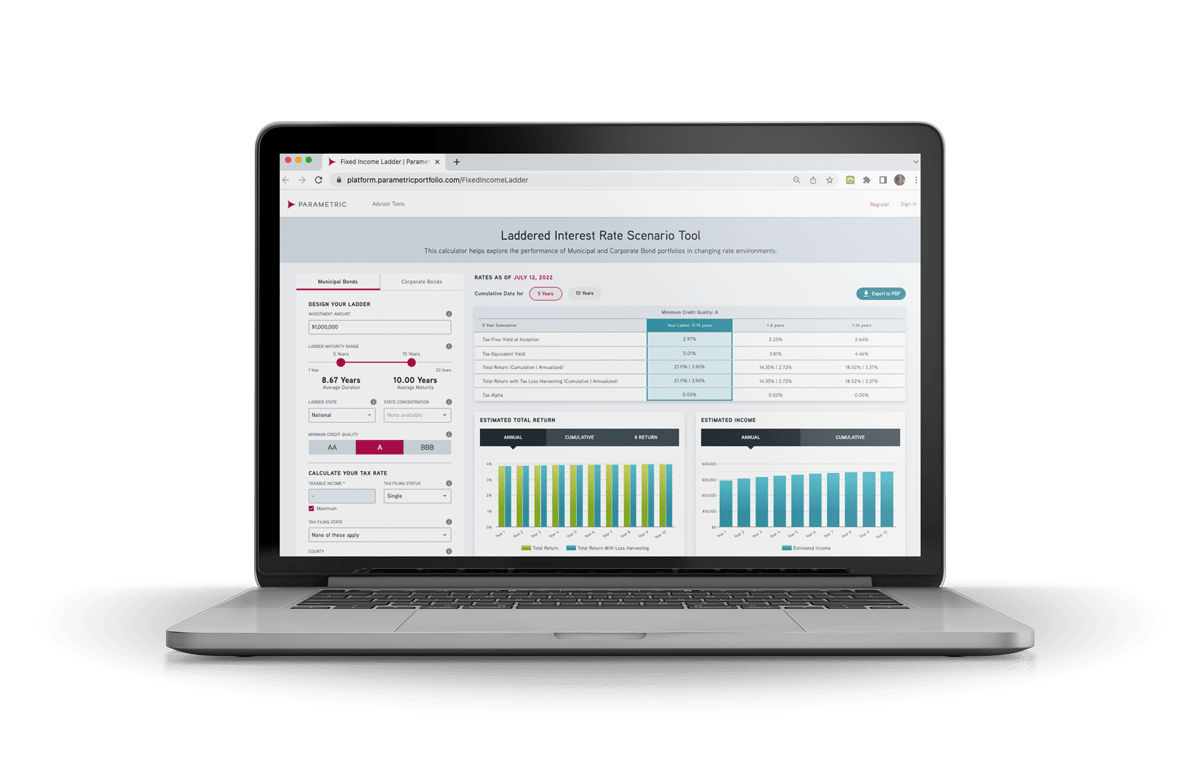

ADVISOR TOOL

Laddered Interest Rate Scenario Tool

Capture the performance of your laddered municipal or corporate bond portfolio in changing rate environments.

Get in touch

Discover how our fixed income solutions can address today’s challenges. Request a sample portfolio or transition analysis.